FDIC & SIPC Protection - What Is It and What Are The Limits?

One of the biggest things I see on social media is people asking about insurance protection on both their bank accounts & investment accounts. Well, no need to worry, because there are two agencies out there that protect your money at the bank and your money in your investment account. Those agencies are the Federal Deposit Insurance Corporation (FDIC) & the Securities Investor Protection Corporation (SIPC).

What is the FDIC?

The Federal Deposit Insurance Corporation (better known as FDIC) is a US government agency that insures deposits in banks and savings associations. You may have seen on your banks website where they have the FDIC logo or wording that says “FDIC insured” at the bottom of the page. This means that bank is covered by FDIC insurance.

In short, the FDIC was created after the Great Depression in 1933 to restore faith in the US Banking system. The purpose of the FDIC is to protect people’s money in the event of a bank failure. You may have heard a lot about FDIC insurance during the Silicon Valley Bank, First Republic Bank and Signature Bank failures in 2023.

Each depositor is insured up to $250,000 per insured bank, per ownership category. Notice a key phrase there, “per ownership category”. This is important because most people think having $250,000 at Capital One means they have no more FDIC insurance at Capital One. However, that is not the case. Since it is based on “per ownership category”, there is a way to get more than $250,000 of coverage at a bank.

Let’s say you have an individual account, you would be protected up to $250,000. Just by doing a joint account, you would be insured up to $500,000 total ($250,000 per owner). So to double the insured amount in coverage at a single bank, you can do a joint bank account.

Another way to do this is to structure accounts in a way that provides additional coverage. For example a married couple could structure their accounts to insure $1 million at a single bank:

Individual account in spouse #1’s name: $250,000 of coverage

Individual account in spouse #2’s name: $250,000 of coverage

Joint account owned by both spouses: $250,000 (for $500,000 total) of coverage

Total FDIC coverage: $1,000,000 for the couple

What the FDIC covers:

Checking accounts

Savings accounts

Money market accounts

Certificates of deposit (CDs)

Cashier's checks and money orders

Negotiable order of withdrawal accounts

What the FDIC does not cover:

Stocks

Bonds

Mutual Funds

Annuities

Life Insurance Policies

Cryptocurrencies

Losses due to theft or fraud

Losses related to currency fluctuations or political risks

When it comes to protecting your money in the bank, FDIC insurance has got you covered (up to the limits).

What is the SIPC?

The Securities Investor Protection Corporation (better known as SIPC) is non-profit organization, created by Congress in 1970, that protects investors from losses at financially troubled brokerage firms. The SIPC is essentially the sibling to the FDIC.

SIPC insurance protects investors for up to $500,000 in securities and up to $250,000 in uninvested cash. However, the total amount of SIPC coverage is $500,000; therefore, if you have $500,000 in securities and $250,000 in cash, that entire amount may not be covered.

Similar to FDIC, there are ways to “get around” the $500,000 limit. For example, if you have a traditional IRA and a Roth IRA at the same brokerage, the SIPC will insure them separately. That means you will be insured up to $1 million between the two accounts.

So for example, if a couple has

Individual account in spouse #1’s name: $500,000 of coverage

Individual account in spouse #2’s name: $500,000 of coverage

Joint account owned by both spouses: $500,000 of coverage

In this case, the couple would have $1.5 million of coverage at the brokerage firm.

What the SIPC covers:

Stocks

Bonds

Treasury securities

Money market mutual funds

Certificates of deposit

Different account types that the SIPC deems as separate (which means you are covered up to $500,000 in each account type):

Individual accounts

Joint accounts

Trust accounts

Corporate accounts

Traditional IRAs and Roth IRAs

Accounts held by an executor of an estate

Accounts held by a legal guardian

What the SIPC does not cover:

Commodity futures contracts (unless they are held in a special portfolio margining account)

Foreign exchange (forex) trades

Fixed annuities contracts

Investment contracts such as limited partnerships

Losses due to market volatility

Losses due to bad investment advice

Losses due to security breach, unless the brokerage becomes insolvent

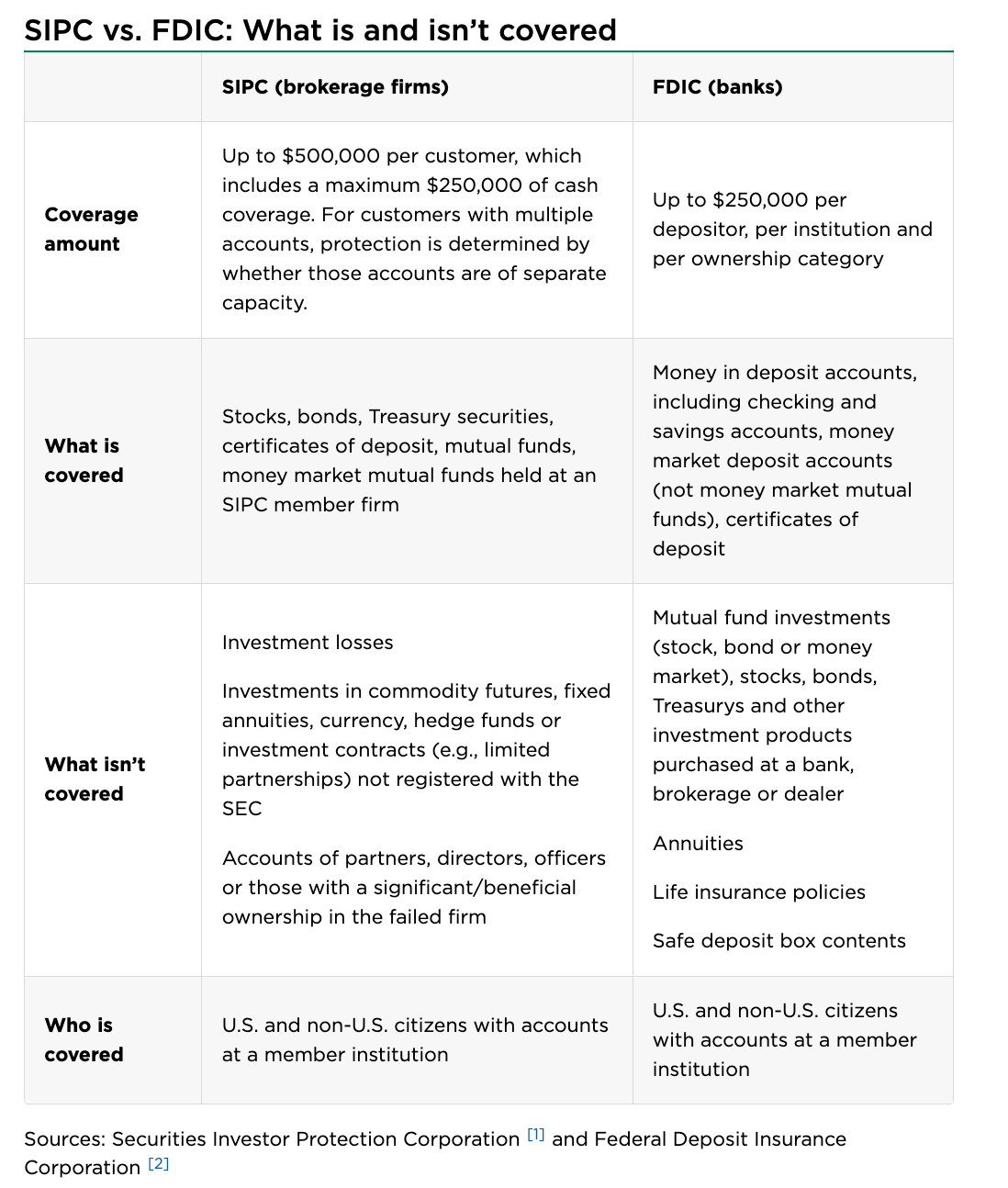

Below is a great image by NerdWallet that lays out the difference between the FDIC & SIPC:

I also want to note that FDIC and SIPC insurance is something that you do not need to “purchase”. By opening an account at an FDIC partnered bank or SIPC partnered broker, then you automatically will be covered by FDIC or SIPC.

I have worked with many clients who have north of $1,000,000+ (some with $10,000,000+) at one custodian & they do not worry about SIPC insurance. Of course it is something to keep in the back of your mind, but I would not let that dictate your investment/banking decisions. If you are holding more than $250,000 in cash, then it is a good idea to either open a different account type OR find another bank to put the additional money over $250,000 in.

Thanks for reading & I hope you found value in this post.

-Kolin

If you are looking to get organized on your finances, read this post: Getting Your Finances Organized As A Newly Married Couple

Disclaimer: The content provided in this blog post is for educational purposes only and should not be considered as financial advice. While every effort has been made to provide accurate and up-to-date information, the content on Money Matters For Two is based on personal research, opinions, and experiences. The financial landscape can change rapidly, and what may be applicable at the time of writing may not necessarily be applicable in the future.

Any financial decisions you make based on the information provided here are entirely at your own risk. Money Matters For Two encourages readers to do their own research and, when necessary, seek the advice of a qualified financial advisor or professional to ensure that any financial choices are appropriate for their individual circumstances.